By Jamie Botha, DataEQ UK Head of Partnerships UK and the Middle East

The Financial Conduct Authority (FCA) recently published a review of firms’ progress in implementing the Consumer Duty regulation, set to come into effect from 31 July 2023.

Applicable to all UK-based firms providing retail financial services, the Duty is intended to raise the bar of care that is expected throughout the customer journey.

In addition to ensuring that all customer communication is of an understandable nature, the Duty aims to ensure that the financial products and services on offer are suitable to meet targeted customers’ needs.

Having reviewed a sample of implementation plans, the FCA sought to establish whether firms were effectively embedding the new regulations within their businesses. Amongst key factors considered here were firms’ data strategies, which should clearly document the customer journey to ensure Consumer Duty compliance.

What does a comprehensive data strategy entail?

“A key part of the Duty is that firms assess, test, understand and evidence the outcomes their customers are receiving. Without this, it will be impossible for firms to know that they are meeting the requirements set out in the Consumer Duty.” – FCA’s multi-firm reviews

In the move towards outcome-based planning, the incoming Consumer Duty rules require firms to document their customer journey in much more detail than before. As such, a firm’s data strategy should clearly outline how they plan to identify, monitor, evidence and stand behind the outcomes that their customers are experiencing.

The data collected, however, needs to be ongoing, which means firms cannot rely solely on historical data. In their identified areas for improvement post-review, the FCA noted that some firms’ data strategies seemed to be largely based on repackaging existing data, with limited consideration of gaps or the outcomes it is intended to monitor.

“If firms assume they can ‘get by’ largely with repackaging or supplementing existing data, then they risk not thinking deeply or afresh about the types and granularity of data that they will actually need to monitor and evidence outcomes under the Duty effectively.” – FCA’s multi-firm reviews

While it is up to each firm to identify suitable data sources as evidence against the outcomes of the Duty, the FCA has gone so far as to outline the types of information that firms should consider collecting in Chapter 11 of their finalised guidance.

Where does social data fit in?

Amongst the types of information that firms should consider including in their data strategies, the FCA has listed “customer feedback” and goes on to explicitly mention comments and complaints made on social media as a viable data source.

“Types of information firms may want to collect include customer feedback. Using formal and informal feedback from customers to identify trends and areas for improvement (e.g. complaints and comments made to the firm but also comments and complaints on social media).”- Final non-Handbook Guidance for firms on the Consumer Duty

Simply collecting this information, however, is not enough to prove that good outcomes are being delivered. The FCA goes on to highlight the importance of “complaints root cause analysis” for investigating complaints fully to understand the cause of customer complaints, and not just dealing with the symptoms.

As an unfiltered source of customer feedback, social media offers a valuable real-time dataset for complaint root analysis, but firms will need to have effective processes and technology in place to enable them to identify and address the various comments and complaints.

Can AI do the trick?

As sophisticated as AI has become, the complexity of informal feedback still confounds machines, which means social media analysis driven purely by machine learning can often deliver inaccurate results. Adding a further layer of complexity is the need to cross-reference evolving market conduct regulations and complaint frameworks.

This raises the question: how will financial firms be able to identify the pertinent customer feedback in an ocean of unstructured online conversation?

One solution is to layer an element of human insight over the analytical work performed by machines. In other words, get real people – “a Crowd” – to refine the work done by AI. Human beings are not only better at dealing with sarcasm and local references, they’re also better at performing granular topic-level analysis required for datasets as diverse as financial services complaints.

What does the data say?

To test the relevance of social media data in the context of market conduct reporting, DataEQ categorised the social conversation and complaints from 15 major UK financial organisations according to the four identified outcomes in the Consumer Duty, using their proprietary technology that combines AI with scaled human intelligence (in the form a Crowd).

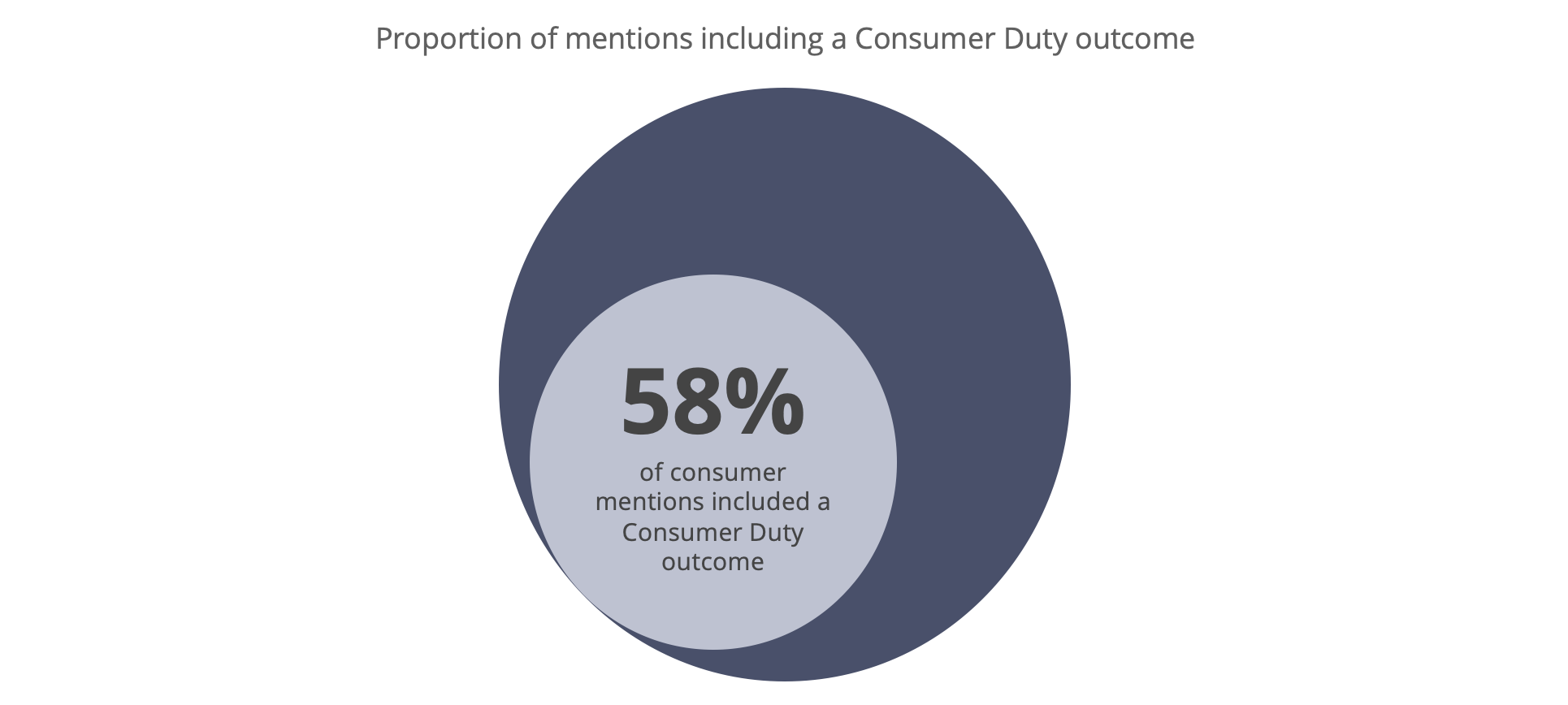

The finding was that over half (58%) of actionable consumer conversation included one or more of the Duty outcomes, revealing that social media data is indeed rich with conduct-related themes.

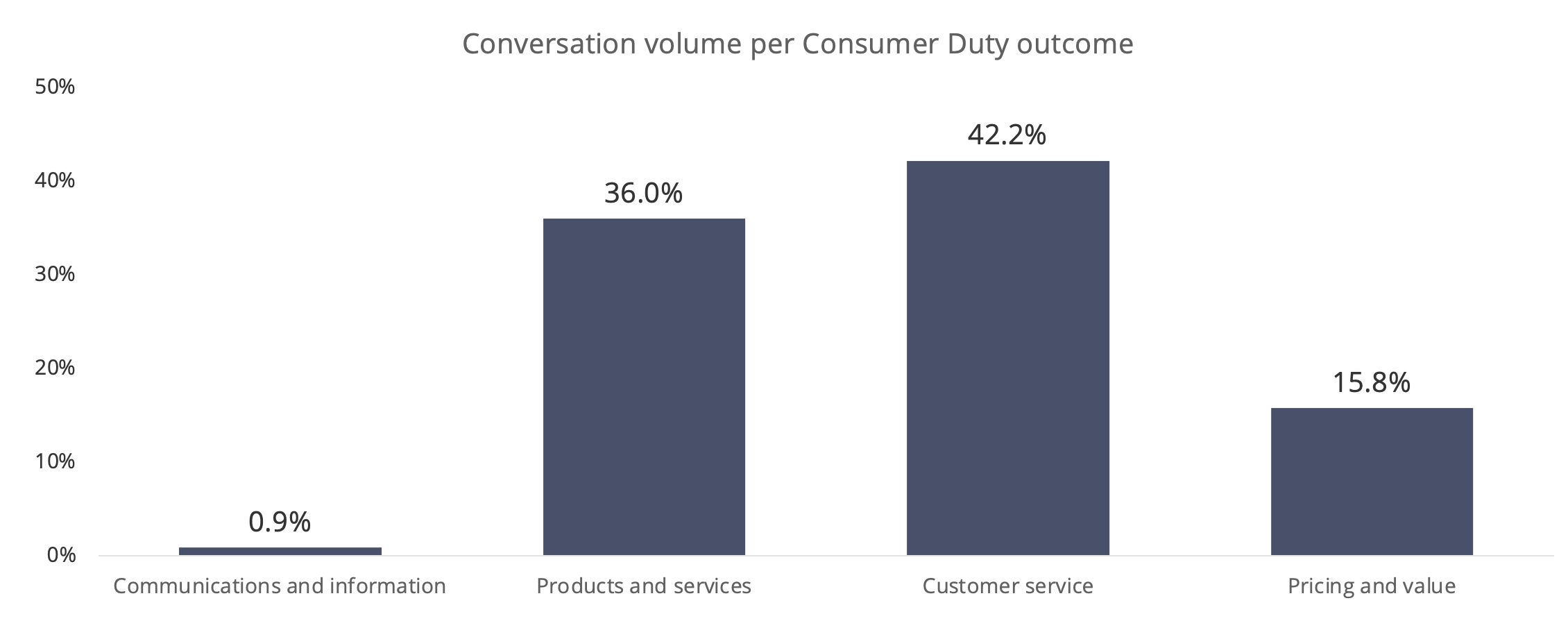

In mapping out the social media conversation across the four outcomes, the bulk of conduct-related complaints related to consumer support (42.2%) and products and services (36%).

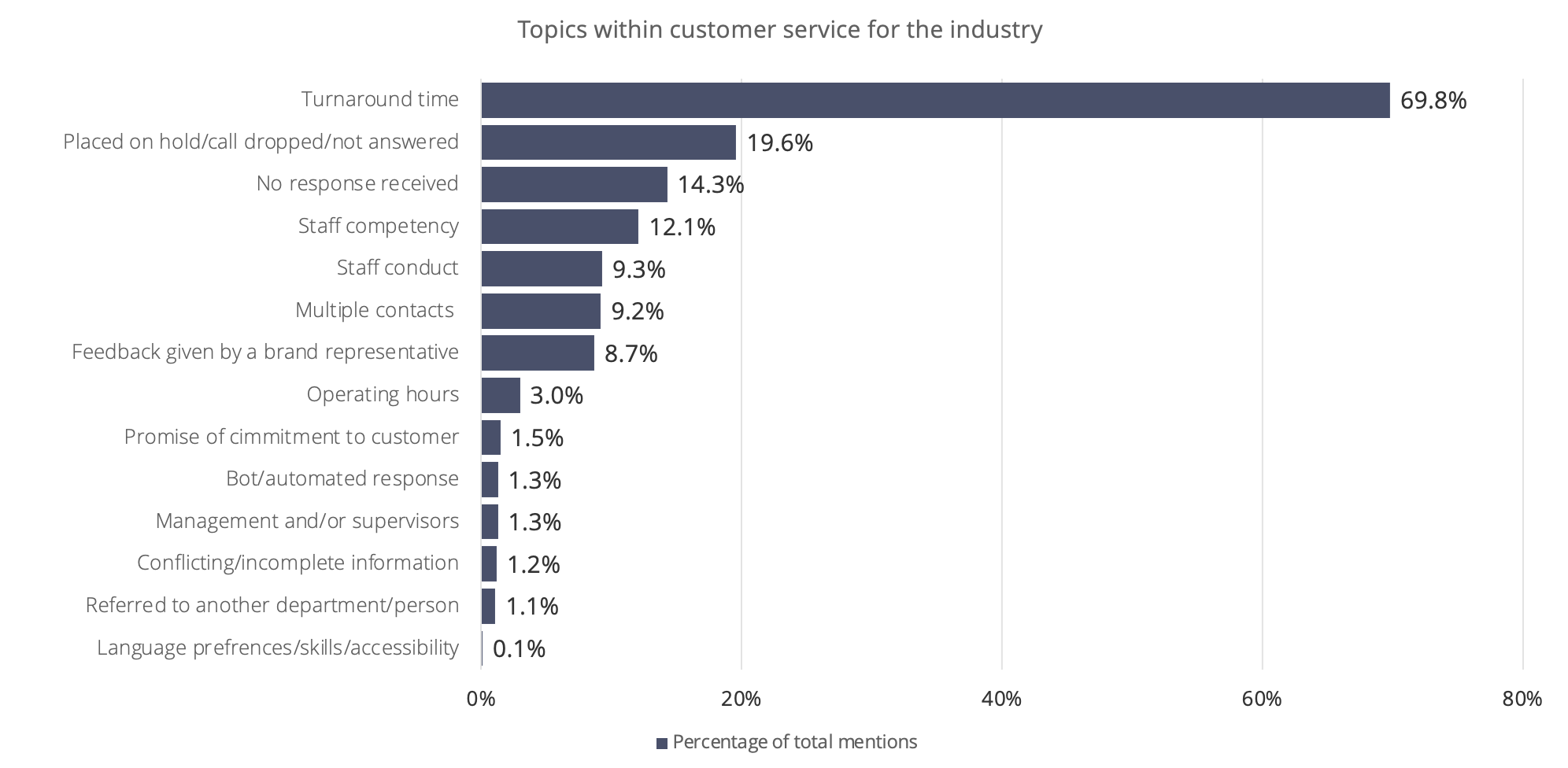

The themes that emerged from service-related conversation showed that expectation management, responsiveness and staff competency are key areas of concern for consumers. Taking this analysis one step further, the data revealed that over two-thirds (69.8%) of consumers speaking about service included a reference to turnaround time for receiving assistance from an organisation.

This analysis supports the notion that social media data is not only relevant in the context of the proposed Consumer Duty, but can also be used to effectively accelerate course correction by proactively signalling areas of potentially bad practice. If captured correctly, social media data can indeed be used to ensure that firms remain customer-focussed in every aspect of their products and service delivery.

The bottom line?

Social media data offers a compelling solution for firms that have yet to tick off the Consumer Duty’s stringent data strategy requirement. Gathering this data, however, is just the first step to evidencing the outcomes that customers are receiving. To achieve this, firms must ensure that they have the necessary social data tools and processes in place to effectively identify, monitor, and stand behind the outcomes that their customers are experiencing.