How insurers are leveraging Trustpilot reviews to drive positivity

DataEQ has released the UK Insurance Sentiment: Consumer Duty Index, which is based on an analysis of over 315,000 posts from X and Trustpilot between 1 July 2023 and 30 June 2024. This report sheds light on whether insurers are meeting customer expectations as outlined by the Consumer Duty guidelines.

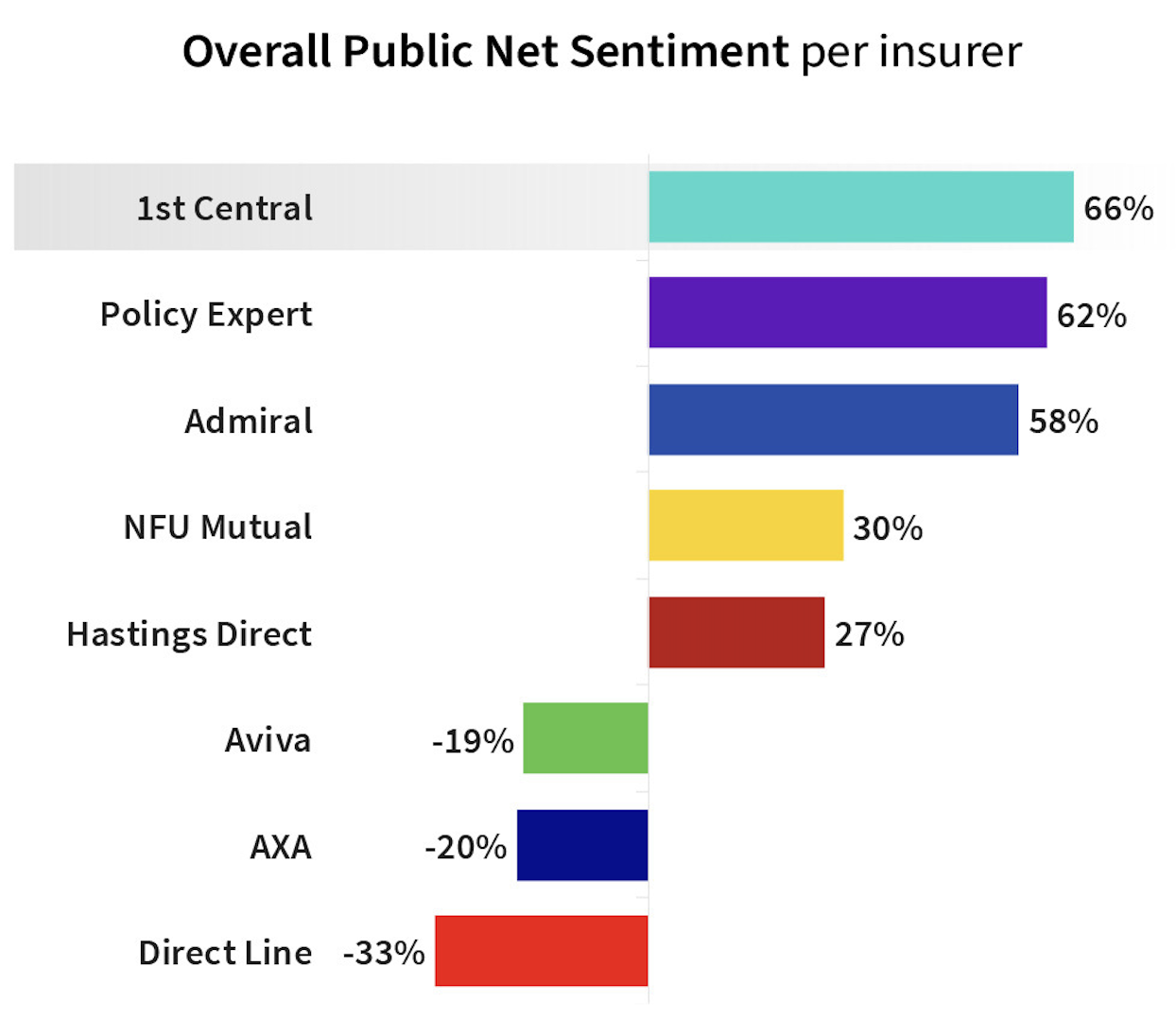

1st Central achieved the highest overall Net Sentiment, with customers praising the insurer for its competitive pricing, user-friendly website, and fast issue resolution. They were followed closely by Policy Expert and Admiral, both of which were also praised for their pricing.

Direct Line was the most negatively discussed insurer, receiving a large number of complaints about unexpected high renewal increases.

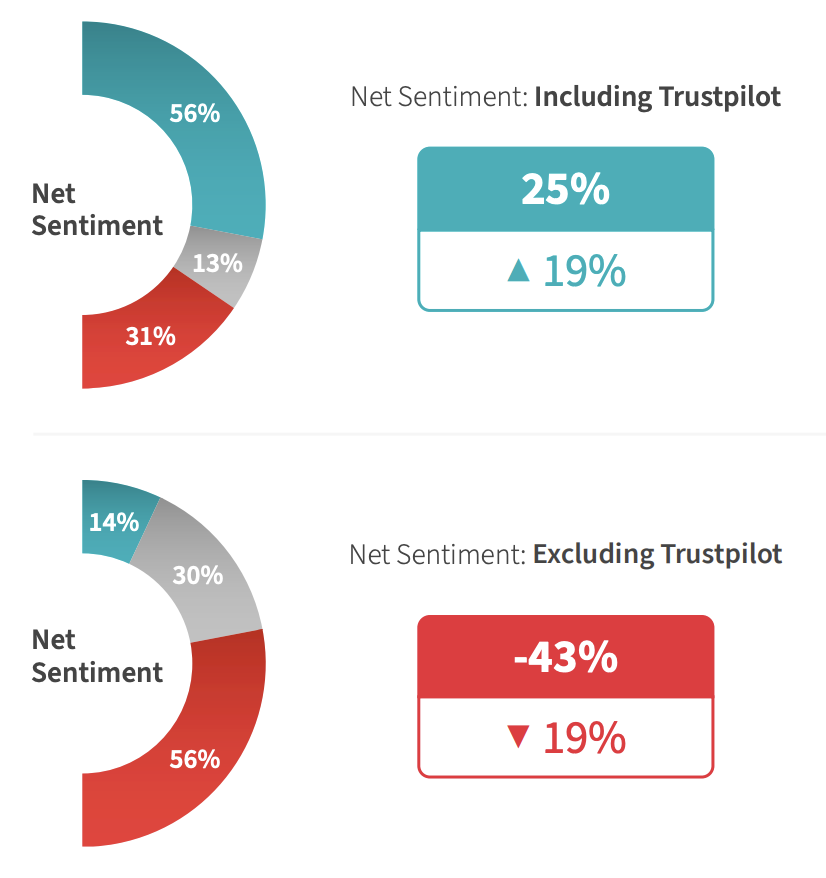

The Trustpilot Effect: Invited reviews drive up industry Net Sentiment

Trustpilot made up nearly two-thirds of total conversation volume and had a major impact on industry positivity, increasing it by 68pp.

60% of this conversation consisted of invited reviews, where customers were asked to share their experiences after dealing with the insurer. These invited reviews were generally positive. In contrast, organic (non-prompted) Trustpilot reviews negatively impacted insurers' Net Sentiment.

Challenges in claims processing and price transparency drove customer frustrations

Customers expressed frustration with prolonged claim resolution times and unexpectedly high premium increases, particularly in motor insurance. These issues were frequently mentioned in unsolicited reviews.

Consumer Duty dominates online conversations

Over half of all online conversations analysed in the report referenced one or more of the Consumer Duty outcomes.

Jamie Botha, Head of Global Partnerships at DataEQ, commented: “The introduction of Consumer Duty has potentially influenced how customers perceive their insurance providers and what they deem is fair. While positive trends are emerging, particularly in transparency and fairness, insurers must remain focused on addressing the operational issues highlighted in unsolicited feedback. Failure to monitor and respond to these conversations could pose significant regulatory risks, as ongoing dissatisfaction may indicate non-compliance with the core principles of Consumer Duty. Insurers need to be proactive in addressing these issues to avoid potential regulatory scrutiny.”